Introduction

The implementation of IFRS 16 has fundamentally changed lease accounting by requiring lessees to recognize right-of-use (ROU) assets and lease liabilities for most leases. This shift has improved financial transparency but introduced complexities in measurement, disclosures, and financial reporting.

For auditors, reviewing compliance with IFRS 16 is critical to ensure organizations correctly apply the standard. This blog explores key areas auditors should focus on, including accounting entries, lease modifications, financial impact, and common audit pitfalls, supplemented with practical examples.

Understanding IFRS 16 and Key Changes

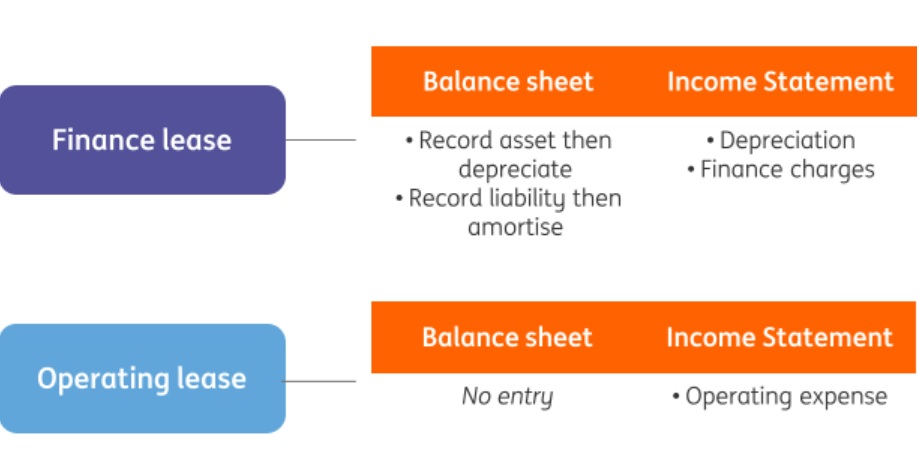

IFRS 16, effective from January 1, 2019, replaced IAS 17 by eliminating the distinction between operating and finance leases for lessees. Instead, all leases are now recorded on the balance sheet, except for short-term leases (≤12 months) and low-value asset leases (≤$5,000).

Major Accounting Changes:

| Aspect | IAS 17 (Old) | IFRS 16 (New) |

|---|---|---|

| Lease Classification | Finance Lease & Operating Lease | All leases recognized on balance sheet (except exemptions) |

| Balance Sheet | Operating leases were off-balance sheet | Leases now recorded as ROU asset & lease liability |

| Income Statement | Straight-line lease expense for operating leases | Depreciation on ROU asset & interest on lease liability |

| Cash Flow Impact | Entire lease payment in operating cash flow | Principal in financing cash flow, interest in operating cash flow |

Example:

Before IFRS 16, a company leasing office space under an operating lease would record rent expense of $50,000 per year. Under IFRS 16, the company now recognizes:

- A right-of-use asset for the present value of lease payments.

- A lease liability, amortized over the lease term.

- Interest and depreciation expenses instead of rent expense.

Essential Accounting Entries under IFRS 16

There are events and transactions happening within a Lease contract over the period of time. Below examples will help you understand the accounting entries from initial recognition to re-assessments and modifications.

Initial Recognition at Lease Commencement

- At the start of the lease, the company records the lease liability and the right-of-use (ROU) asset.

Journal Entry:

Dr. Right-of-Use Asset (ROU) $500,000

Cr. Lease Liability $500,000

The lease liability is calculated as the present value of future lease payments, discounted at the lessee’s incremental borrowing rate.

Subsequent Recognition

- Monthly interest and principal repayment affect lease liability.

- Depreciation is recorded on the ROU asset.

Journal Entry for Monthly Lease Payment ($10,000)

Dr. Lease Liability $6,000

Dr. Interest Expense $4,000

Cr. Cash/Bank $10,000

Journal Entry for Depreciation (assuming 10-year lease life)

Dr. Depreciation Expense $50,000

Cr. Accumulated Depreciation – ROU $50,000

Lease Modifications & Reassessments

- Changes in lease term, rent adjustments, or scope require reassessment.

- New discount rate may be applied for modifications.

Example:

If a lessee extends the lease term from 5 years to 7 years, the lease liability is remeasured using a revised discount rate.

Dr. Right-of-Use Asset (adjustment) $100,000

Cr. Lease Liability $100,000Auditor’s Key Focus Areas in Reviewing IFRS 16

Below are the key focus areas for an auditor while reviewing IFRS 16 / Leases in any organization.

Lease Identification & Completeness

- Review contracts to ensure all lease components are identified.

- Check for embedded leases (e.g., leases hidden in service contracts).

- Common Pitfall: Companies may fail to identify all lease obligations, leading to underreporting of liabilities.

Discount Rate Accuracy

- Validate the incremental borrowing rate (IBR) used to discount lease payments.

- Common Pitfall: Using an incorrect discount rate significantly impacts liability valuation.

Correct Depreciation & Interest Expense Calculation

- Verify depreciation matches lease term and interest reduces liability appropriately.

- Common Pitfall: Some companies continue expensing leases incorrectly instead of applying depreciation and interest.

Lease Modifications & Adjustments

- Confirm that lease changes (e.g., extensions, rent increases) are properly remeasured.

- Common Pitfall: Failure to update lease liabilities when lease terms change.

Financial Statement Disclosures

- Review disclosures for lease maturities, variable lease payments, and significant judgments.

- Common Pitfall: Missing disclosure of lease commitments and assumptions.

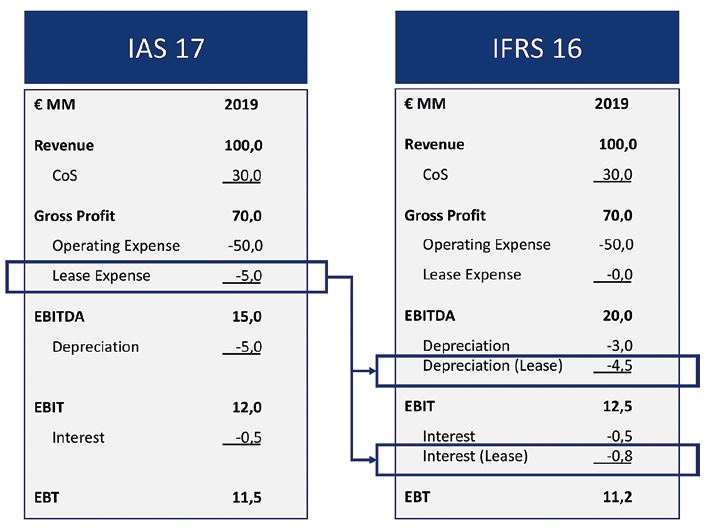

Impact of IFRS 16 on Financial Reporting

| Financial Statement | Impact Under IFRS 16 |

|---|---|

| Balance Sheet | Increased assets (ROU) & liabilities (lease liability) |

| Income Statement | Higher EBITDA, but lower net income in early years due to front-loaded interest |

| Cash Flow Statement | Lease principal payments shift to financing activities, improving operating cash flow |

Example:

A retail company previously reporting $2M in rent expense under IAS 17 now records:

- Depreciation ($1.5M) on ROU asset

- Interest expense ($600K) on lease liability

- Net impact: Higher EBITDA but a front-loaded expense pattern

Conclusion

IFRS 16 has revolutionized lease accounting, making financial statements more transparent but also more complex. Auditors must ensure accurate recognition, measurement, and disclosure of lease obligations.

Key Takeaways for Auditors:

✔ Ensure all leases are identified and correctly classified.

✔ Validate discount rates and present value calculations.

✔ Check lease modifications for accurate adjustments.

✔ Review financial disclosures for completeness.

By applying a thorough review process, auditors can help organizations comply with IFRS 16 and improve financial reporting accuracy.

References

- IFRS Foundation. “Effects Analysis of IFRS 16.” (IFRS.org)

- FinQuery. “IFRS 16 Leases: Summary, Examples, and Journal Entries.” (finquery.com)

- Nakisa. “Year-End Audit Procedures for IFRS 16 Compliance.” (nakisa.com)

- Occupier. “Lease Audit Procedures: Best Practices.” (occupier.com)